Singapore Real Estate & Property Market Prices 2024: Expert Forecasts & Analysis by Zach Lin

As Singapore navigates through dynamic changes in the global economic landscape, the real estate and property market remains a key area of focus for investors, homebuyers, and market analysts alike. This comprehensive guide delves into the trends, future outlook, and driving factors of property prices in Singapore for the rest of 2024.

Current Price Trends in the Singapore Property Market

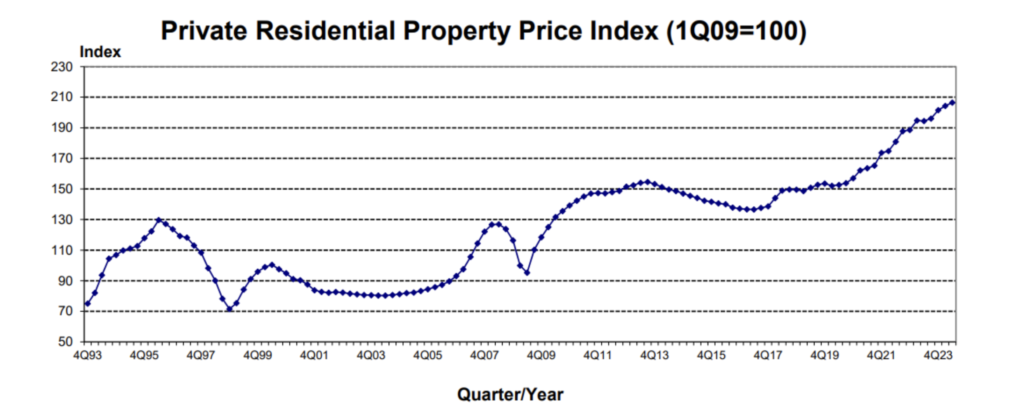

In 2024, the Singapore real estate and property market is characterised by strong activity, reflecting a combination of economic resilience and evolving market challenges. Influential factors driving up Singapore property prices include a constrained housing supply, elevated interest rates, and robust foreign investment. According to the Urban Redevelopment Authority (URA), the overall private home price index is on the positive side for both Q1 and Q2.

Source: URA

However, in the first quarter of 2024, private home prices in Singapore rose by 1.4%, a slowdown from the 2.8% increase in Q4 2023, marking the slowest quarterly gain since Q3 2021. This trend continued into the second quarter of 2024, where Singapore property prices grew at a slower pace of 1.1%, down from 1.4% in Q1. Despite these modest increases, property prices have surged by 49.6% since a low in Q2 2017, demonstrating the resilience of the Singapore property market.

Median transacted prices of new non-landed private homes dropped by 1.5% to $2,238 psf (per square foot) in Q2, while resale prices increased by 2.1% to $1,709 psf. This reflects a growing shift towards more affordable secondary market options as buyers become more selective, particularly in high-end properties.

Insights on Market Dynamics in 2024

Let’s take a deeper look at the nuanced analysis of the dynamics shaping the property prices in Singapore. The current market dynamics balance the effects of stringent government cooling measures against a renewed surge in foreign demand. Despite declining sales figures and moderating price growth in 2023, property owners demonstrated resilience, with no urgency to sell and maintaining high asking prices, even in prime districts like the CCR (Core Central Region).

This underscores the critical role of government cooling measures in Singapore’s real estate and property market, which are designed to temper market overheating effectively. Recent data shows that these measures have helped to decrease the rate of price growth in Singapore from 6% in previous years to a more sustainable estimate around 3% this year. In the first half of 2024, the Government Land Sales (GLS) programme released 5,450 units, the highest supply on the confirmed list since 2H 2013, aimed at maintaining price stability.

Forecasting Singapore Property Prices

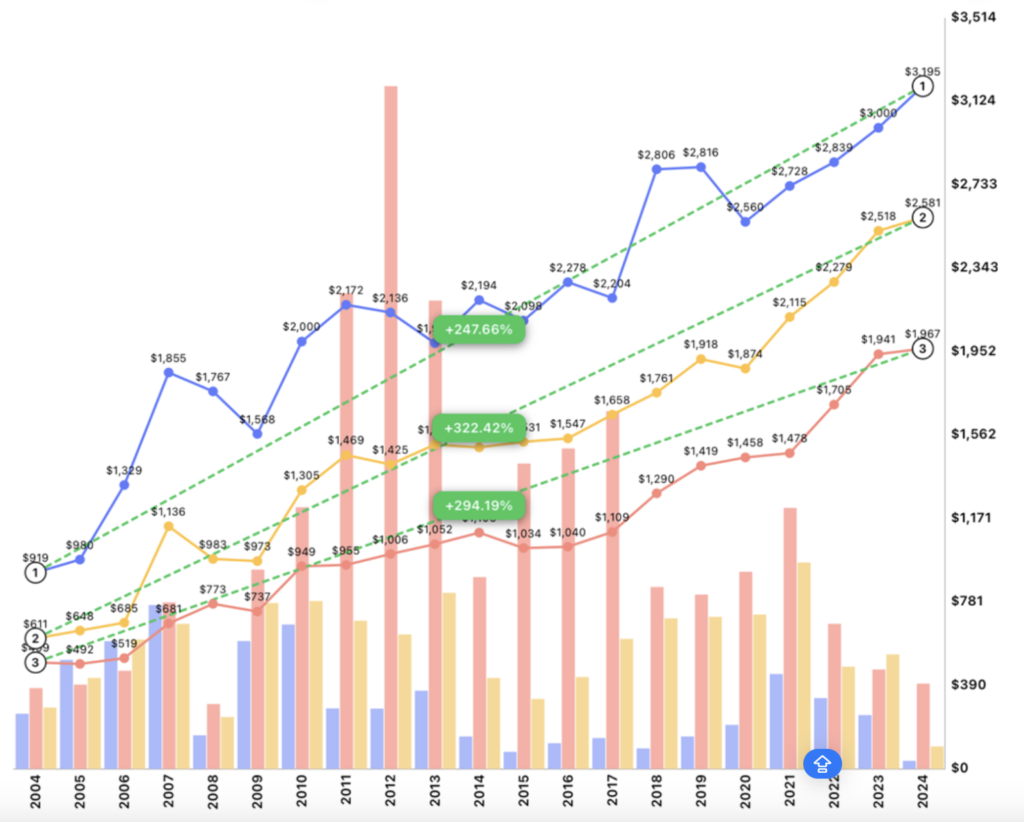

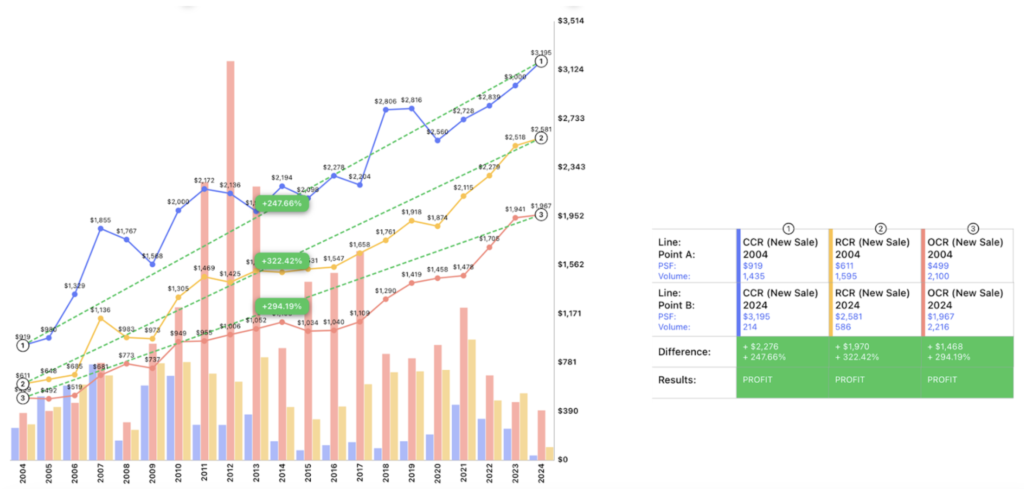

Moving forward, it is likely to see a steady increase in property prices in Singapore into the next year. Anticipated factors include continuous infrastructure enhancements, the entry of global tech corporations into Singapore, and limited new residential unit releases. New private property launch prices in Singapore are expected to remain around $1,967 psf for OCR (Outside Central Region) , $2,581 psf for RCR (Rest of Central Region), $3,195 psf for CCR, while Executive Condominium (EC) prices are anticipated to range between $1,450 and $1,550 psf. Despite potential upward price pressures, existing cooling measures should aid in sustaining balanced growth. Industry forecasts suggest that prices may rise by up to 4% in the coming year, driven primarily by demand in prime districts.

Market Activity and Buyer Shifts in the Singapore Housing Market

Developers launched 1,304 uncompleted private residential units in Q1 2024, up from 1,060 in the previous quarter. However, new private home sales (excluding ECs) fell by 41.4% in Q2 to 679 units, down from 1,158 in Q1, while resale transactions increased by 8.1% to 3,073 units. This shift towards the resale market reflects buyers seeking more affordable options as high-end properties, particularly in prime districts, faced price declines or stagnation due to lower foreign demand and increased selectivity among local buyers.

Key Factors Impacting Property Prices in Singapore

The Singapore real estate and property market is influenced by multiple pivotal elements:

- Economic Conditions and Interest Rates: With ongoing economic uncertainty in Singapore and potential delays in interest rate cuts, property seekers are likely to gravitate toward homes offering better value, with many adopting a wait-and-see approach. Despite these challenges, sales activity in Singapore’s property market is expected to stabilise, primarily driven by owner-occupiers. However, affluent investors in Singapore may still explore opportunities to acquire second properties.

- Buyer Behaviour: A noticeable shift towards properties in the OCR, particularly those near MRT stations due to their better value proposition compared to CCR properties, is anticipated. Additionally, there is a growing trend of buyers opting for larger HDB flats or those located in prime areas. For instance, in Q1 2024, landed property prices increased by 2.6%, while non-landed homes saw a 1% rise. Non-landed property prices in the CCR increased by 3.4%, while the RCR and OCR saw smaller increases of 0.3% and 0.2%, respectively.

- Government Interventions: The Government Land Sales (GLS) programme’s release of 5,450 units in the first half of 2024 is a key example of interventions aimed at maintaining market stability. Despite these efforts, developers may sell up to 7,000 new homes in 2024, with total resale and sub-sale transactions projected between 12,000 and 13,000 units.

- Economic Growth: Singapore’s robust economic expansion continues to significantly bolster property demand. According to the Ministry of Trade and Industry Singapore (MTI), the economy experienced a notable growth of 2.9% on a year-on-year basis in Q2 2024. This strong performance is part of the broader Singapore economic growth 2024 trend, with MTI projecting a sustained growth rate of 1 - 3% for the full year. The IMF projects Singapore’s economy to grow by 2.1% in 2024, an improvement from 1.0% in 2023, which may support property market resilience, despite global challenges like high interest rates and economic uncertainty. A shift of individuals from the middle-income bracket to the higher-income bracket, coupled with the growth of the middle class, is expected to support property prices.

- Population Trends: Demographic shifts and a steady population growth rate of approximately 0.60% per year continue to drive demand for housing in Singapore. These trends are crucial for understanding the dynamics within the Singapore property market, as they directly influence both the residential and commercial sectors, underscoring the ongoing need for diverse real estate investments.

Market Outlook for Singapore Property Prices

Analysts expect private home prices in Singapore to rise by 4% to 6% year-on-year by Q4 2024. Despite some expected price stability, challenges such as fragmented supply chains, sustainability considerations, and persistently high interest rates are likely to keep new home prices elevated, especially in the CCR. These factors contribute to the overall resilience of the market, as buyers adjust to new economic realities while seeking the best value in their property investments.

Conclusion

Looking ahead into 2024, the Singapore real estate and property market offers numerous opportunities amidst its inherent challenges. By being well-informed and understanding the market's foundational forces, investors and homebuyers are better equipped to make savvy decisions.

Partnering with industry professionals like Zach Lin can greatly enhance your ability to navigate this dynamic market. As Zach advises, “Success in this market comes from understanding its cyclical nature, timing your entry and exit points correctly, focusing on long-term trends rather than short-term anomalies, and staying up-to-date with policy changes.” Contact Zach below for more insights today.