Singapore Real Estate and Property Market 2024: Key Insights and Emerging Trends by Zach Lin

Singapore's property market remains a hotspot for luxury living, offering unparalleled convenience and cultural richness. This article spotlights three exceptional condominium launches in Q3, each presenting unique advantages and lifestyle upgrades in key districts: Meyer Blue, Emerald of Katong, and Chuan Park.

Meyer Blue: A Lifestyle Upgrade in District 15

Economic Stability and Growth

Meyer Blue, located on prestigious Meyer Road, is a freehold condominium offering prime East Coast living. With breathtaking views and seamless access to top schools and retail destinations, this development epitomizes luxury and convenience in Singapore’s real estate market. This is more than just a home—it's a refined lifestyle upgrade.

Key Features

Freehold Tenure: Secure long-term value in a coveted area.

Prime Location: 6-minute walk to Katong Park MRT, connecting to CBD and Changi Airport.

Unrivaled Views: Enjoy exclusive, unobstructed city skyline, sea, and landed estate views.

Comprehensive Amenities: A haven for lifestyle aficionados, with close proximity to East Coast Park, diverse dining, and prestigious schools.

In the Proximity

Schools: Chung Cheng High School (0.98 km), Dunman High School (1.04 km), Tanjong Katong Primary School (1.34 km).

MRT Stations: Katong Park MRT (0.63 km), Tanjong Katong MRT (0.7 km), Dakota MRT (2.8 km).

Supermarkets: Makena’s Mart (0.34 km), FairPrice Xpress (1.0 km), FairPrice Jalan Tiga (2.2 km).

Parks: Katong Park (0.61 km), Wilkinson Interim Park (1.3 km), Arthur Park (1.3 km).

Malls: i12 Katong, Parkway Parade & more

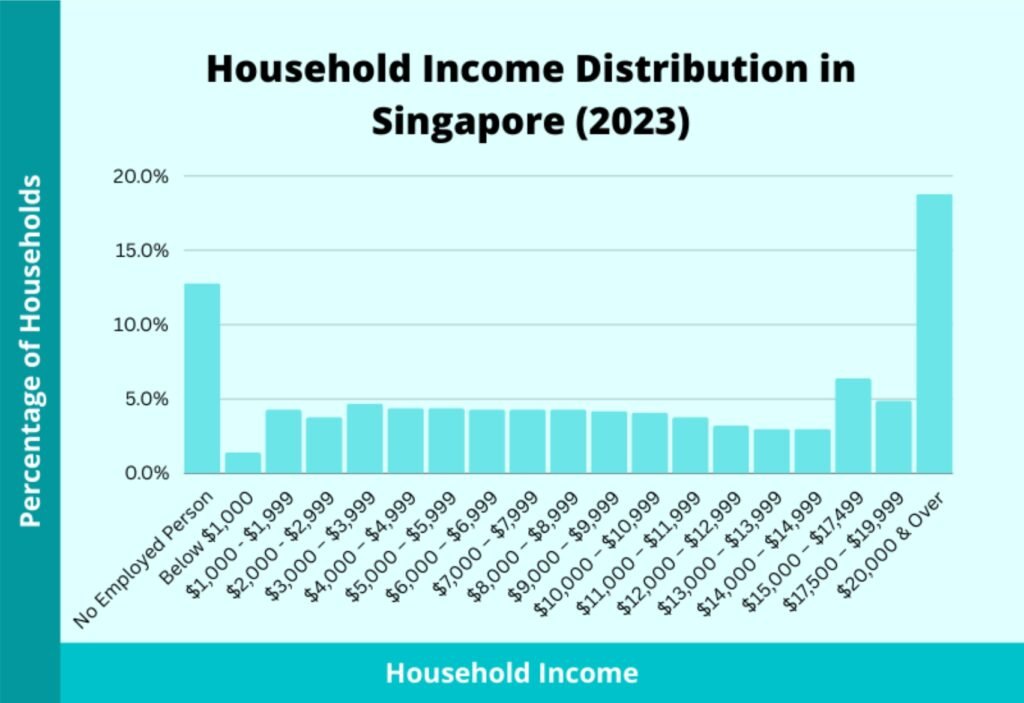

Between 2021 and 2023, the percentage of resident households earning $8,000 and above increased from 51.1% to 55.7%. Additionally, households earning $20,000 and above climbed from 14.4% to 18.8%. This general rise in income levels is offset slightly by an increase in households with no employed persons, which grew from 11.8% to 12.8%. This shift in income dynamics underscores the growing purchasing power among Singaporean households, further driving demand in the property market.

Source: The Straits Times

2. Government Policies and Regulations

To stabilise property prices, the Singapore government introduced additional cooling measures starting in September 2022, with further adjustments in 2023 and 2024. These measures are designed to curb speculative investments and ensure that HDB resale flats remain affordable for buyers. Key regulations include:

15-Month Waiting Period: Private property owners must wait 15 months after selling their property before purchasing a non-subsidised HDB resale flat.

Loan-to-Value (LTV) Limit: The LTV limit for HDB loans has been reduced from 80% to 75%, promoting greater financial prudence.

Additional Buyer’s Stamp Duty (ABSD): Rates have increased to further discourage speculative buying, with higher percentages for second and subsequent properties.

| Additional Buyer’s Stamp Duty for Residential Property | Current Rates effective 27 April 2023 |

|---|---|

| Singapore Citizens |

First Property: 0% (Unchanged) Second Property: 20% (Revised from 17%) Third Property & Onwards: 30% (Revised from 25%) |

| Permanent Residents |

First Property: 5% (Unchanged) Second Property: 30% (Revised from 25%) Third Property & Onwards: 35% (Revised from 30%) |

| Foreigners | Any Property: 60% (Revised from 30%) |

| Entities | Any Property: 65% (Revised from 35%) |

| Trustees | Any Property: 65% (Revised from 35%) |

| Housing Developers | Any Property: 35% remittable, subject to conditions + 5% non-remittable (Unchanged) |

Housing Grants and Schemes in Singapore

Enhanced grants, such as the Enhanced CPF Housing Grant (EHG) and the Fresh Start Housing Scheme, continue to support first-time buyers and families, stabilising the HDB resale market and contributing to broader real estate trends in Singapore.

New HDB Classification Framework

The Housing and Development Board (HDB) introduced a new classification framework for Build-to-Order (BTO) flats, including stricter sale conditions such as a 10-year Minimum Occupation Period (MOP) and an income ceiling for resale buyers. This framework aims to keep flats affordable and ensure they serve as homes rather than vehicles for profit.

Resale buyers of Plus and Prime flats will also encounter a 10-year MOP and an income ceiling of $14,000 for both families and singles. Additionally, those downgrading from private property must wait 30 months after selling before they can apply for Plus or Prime BTO flats. Furthermore, owners will be subject to subsidy clawback upon selling their flat.

Impact of New HDB Classification in Singapore

The new HDB Classification Framework may lead to increased demand for Standard flats due to restrictions on Plus and Prime flats, potentially driving up prices. Stricter rules, such as the October 2023 regulation barring applicants from reapplying if they decline unit offers, could shift interest towards resale HDB flats, further influencing market trends.

3. Demand and Supply Dynamics

BTO Category

Standard

Location

All locations, applies to most flats

Restrictions

● 5-year Minimum Occupation Period (MOP)

Subsidies

Standard

BTO Category

Plus (from H2 2024)

Location

Choice locations within regions (e.g., near MRT stations, town centres)

Restrictions

● 10-year MOP

● Subsidy recovery upon resale (lower than Prime)

● Some BTO eligibility conditions on resale, including income ceiling

● More details to come

● Subsidy recovery upon resale (lower than Prime)

● Some BTO eligibility conditions on resale, including income ceiling

● More details to come

Subsidies

High

BTO Category

Prime (from Nov 2021)

Location

Choicest and most central locations (e.g., city centre, Greater Southern Waterfront)

Restrictions

● 10-year MOP

● Subsidy recovery upon resale

● No whole flat rental

● Full BTO eligibility conditions on resale, including income ceiling ($14k for couples, $7k for singles)

● Subsidy recovery upon resale

● No whole flat rental

● Full BTO eligibility conditions on resale, including income ceiling ($14k for couples, $7k for singles)

Subsidies

Highest

Private Residential Market Outlook in Singapore

Despite subdued home sales due to limited new project launches, private residential property prices continued to rise in Q2 2024, albeit at a slower pace. For the full year 2024, private home prices are expected to increase by 4% to 5%, down from a 6.8% rise in 2023. Many homebuyers are holding out for new projects later in the year, indicating strong interest but a preference for more options before making decisions.

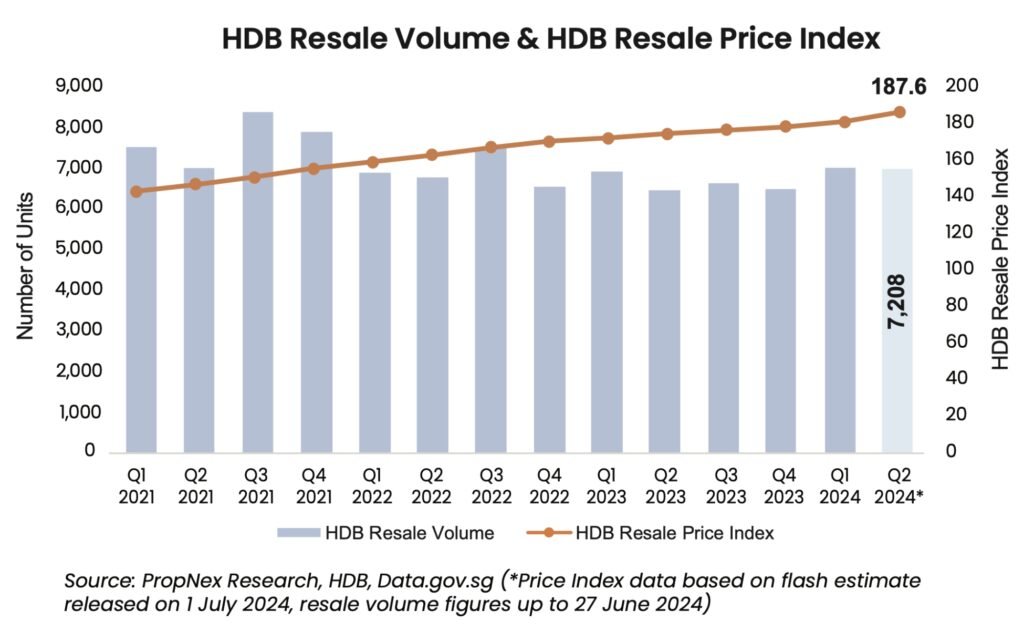

HDB Market Outlook in Singapore

HDB resale prices have stabilised following the significant double-digit growth seen in 2021 and 2022. The first half of 2024 has seen an increase in million-dollar HDB flat transactions, likely driven by former private homeowners re-entering the market after the 15-month wait-out period introduced in September 2022. Demand for HDB resale flats is expected to remain robust, with overall prices projected to rise by 6% to 7% in 2024.

New Residential Projects

The government’s Land Sales Programme is set to introduce several new residential projects in 2024, balancing supply to meet growing demand and maintaining stability in the Singapore real estate market.

Integration of Technology

4. Technological Advancements in Real Estate

Technology continues to transform the Singapore real estate sector with online video tours, digital marketing, and AI-driven property valuation. These tools are becoming increasingly prevalent, enhancing client services and decision-making and reflecting the growing importance of real estate technology in Singapore.

5. Other Market Segments: Commercial and Industrial

Commercial Real Estate

Demand for office spaces in prime locations continues to grow, particularly for flexible and co-working environments. Businesses are expanding and adapting to new work trends, influencing the commercial real estate trends in Singapore.

Industrial Real Estate

The rise of e-commerce has spurred increased interest in industrial properties, especially in logistics and warehousing sectors. Areas like Jurong and Tuas are seeing significant developments to cater to this demand, reflecting the industrial property demand in Singapore.

Focus on Green Initiatives

6. Sustainability and Green Buildings

Sustainability is a growing priority in real estate and property development. Expect to see more green buildings and eco-friendly developments in Singapore as developers and buyers align with Singapore’s vision for a greener urban environment. Initiatives like the Green Mark Scheme and the Sustainable Singapore Blueprint support these efforts as Singapore ventures into sustainable real estate and property.

Investment Opportunities

Zach Lin’s Insights: Navigating Singapore’s Property Investment Opportunities

Emerging hotspots with high growth potential include areas like Punggol, Tengah, Woodlands, and Woodleigh, driven by significant urban development projects. These regions are marked as promising investment zones for those looking to expand their portfolios in Singapore.

Market Navigation Strategies

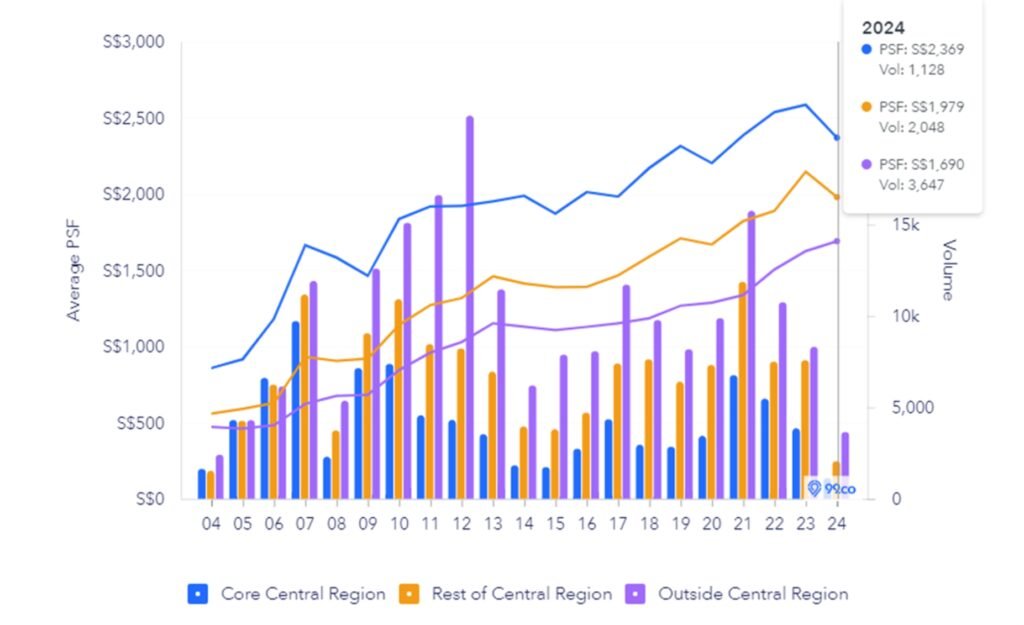

Navigating the complexities of the Singapore real estate market requires leveraging exclusive tools, insights, and resources. By staying ahead of property valuation trends and complying with legal requirements, you can make informed decisions. Analysing blended PSF (Price Per Square Foot) across the CCR, RCR, and OCR districts, we identify the best investment opportunities for both investors and homebuyers.

Conclusion

As we continue through 2024, the Singapore real estate and property market presents a mix of opportunities and challenges. Keeping updated on market trends, government policies, and technological advancements is crucial for informed decision-making in real estate and property investments.